Hot property: an easy-to-follow guide to capital gains

If you find the rules around capital gains on UK property a little hard to follow, our tax technician Trisha Doan is here to demystify things.

Capital Gains Tax on Property – Key takeaways

- CGT is paid on the profit when selling property (not the sale price)

- Applies to buy-to-lets, second homes, and inherited property

- Main homes are usually exempt (Private Residence Relief)

- You can deduct costs like legal fees and improvements

- You must report and pay within 60 days

First things first. What do we even mean by Capital Gains Tax (CGT)?

Essentially it's a tax on the profit you make when you sell a range of things – shares, business assets, or valuable personal items such as artwork or jewellery, for example. Here, I want to focus on its specific application to the world of property.

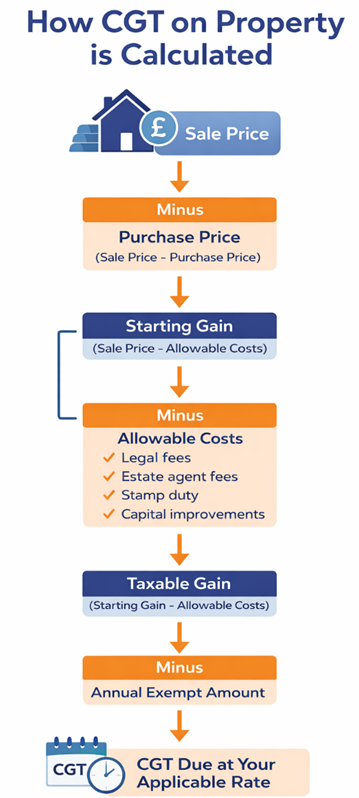

Sometimes people get confused, thinking the capital gain is based on sale price alone or the full amount you receive. Actually, we arrive at the taxable figure by taking the sale price of the property minus what you paid for it and minus certain allowable costs.

When does the tax apply?

You usually pay CGT on a buy-to-let property or second home. It can also apply to an inherited property if it increases in value over time. Because of Private Residence Relief, you don't pay CGT when selling your main home.

What counts as profit?

It's best to think of a real-world example here. Let's say you bought a flat for £200,000, but sell it for £300,000, then your 'starting gain' is £100,000. You are, however, entitled to deduct legal fees when buying and selling, estate agency fees, the stamp duty paid when buying, and what would be described as 'capital improvements' (not routine repairs, but something like a loft conversion or extension). So the actual amount on which you pay tax may turn out to be lower than the £100k.

There is also an annual tax-free allowance called the Annual Exempt Amount, with married couples and civil partners able to use both their allowances.

|

Item

|

Amount (£)

|

|

Purchase Price

|

200,000

|

|

Sale Price

|

300,000

|

|

Initial Gain

|

100,000

|

|

Legal & Estate Agent Fees

|

-5,000

|

|

Stamp Duty

|

-3,000

|

|

Improvements

|

-10,000

|

|

Taxable Gain

|

82,000

|

What rate of tax do you pay?

The rate depends on your income and whether you're a basic-rate or higher-rate tax payer. You can check out the current rates here.

How does inheritance work?

If you inherit a property, you don't pay CGT at that point. You acquire it at the probate value and, then, if you sell it for more than that price, you're liable for CGT on the increase.

When do you have to pay?

Normally the tax needs to be reported and paid within 60 days of a sale going through, so make sure you don't get caught out.

Hopefully, I've been able to clarify some of the most common questions about CGT, but it's a complex area and proper advice is always advisable. If you'd like to speak to an expert at Page Kirk, please call us on 0115 955 5500 or email enquiries@pagekirk.co.uk.

Click here to find out more about our capital gains tax services

Click here to find out more about our property tax services

Frequently Asked Questions

- Do I pay CGT on my main home?

No, due to Private Residence Relief.

- How quickly do I need to report CGT?

Within 60 days of completion.

- Can I reduce my CGT bill?

Yes, by deducting allowable costs and using your annual exemption.

Fact-checked and up to date

Verified

Published: March 2026

The Page Kirk team is committed to providing content that adheres the highest standards for accuracy. We evaluate how the content of each article aligns with current financial procedures and standards. Therefore, the information presented in this article is accurate and up to date.